New Construction or Substantial Rehabilitation

FHA 221(d)(4) Term Sheet

We are obsessed with quality and perpetual improvement. As we get to know you, our approach will be optimized and tailored toward your transactional objectives.

Loan Term

40 years

Interest Rate

Fixed rate, fully amortizing

Non-recourse

Non-recourse

Assumable

Fully assumable

Prepayment

10% year one, then declining 1% per year; and customizable

Commercial Space

No commercial space greater than 25% of net rentable area and 20% of effective gross income of the property

Borrower

A single asset SPE

Escrows

Prior to construction, reserves for interest, insurance, taxes, working capital, and initial operating deficit must be established. These balances will be released to the borrower following six consecutive months of break-even operations. Post construction, insurance, taxes, and MIP will be escrowed monthly. Additionally, a capital needs reserve will be maintained with monthly deposits in accordance with HUD guidelines on a property specific basis.

Davis Bacon Wages

Payment of prevailing wages for contractors and subcontractors

Third Party Reports

Market Study, Appraisal, Environmental Report, future Capital Needs Assessment and an Architectural and Cost Review

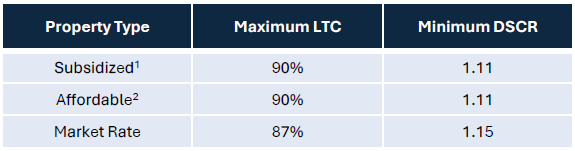

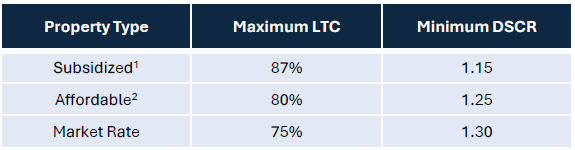

DSCR/LTV Requirements: For Loan Amounts of $130 Million and Above

Mortgage Insurance Premium: 0.25% due at closing and annually thereafter

- At least 90% of the units covered by a project-based Section 8 contract for at least 15 years.

- Regulatory Agreement in place with minimum set-aside (e.g., 40% of units at 60% AMI, or 20 % of units at 50% AMI) in effect for at least 15 years

Connect with an Expert

Grow with Bravo

Grow with Bravo

Grow with Bravo

Grow with Bravo

Grow with Bravo

Grow with Bravo